diff --git a/01 Cloud Platform/10 Live Trading/03 Data Feeds/01 US Equities/03 Universe Selection.php b/01 Cloud Platform/10 Live Trading/03 Data Feeds/01 US Equities/03 Universe Selection.php

index 6f98429966..23b97fac04 100644

--- a/01 Cloud Platform/10 Live Trading/03 Data Feeds/01 US Equities/03 Universe Selection.php

+++ b/01 Cloud Platform/10 Live Trading/03 Data Feeds/01 US Equities/03 Universe Selection.php

@@ -1,14 +1,14 @@

The US Equities data feed enables you to create a dynamic universe of securities.

The US Equities data feed enables you to create a universe of securities to match the constituents of an ETF. For more information about ETF universes, see ETF Constituents Selection .

+

The US Equities data feed enables you to create a universe of securities to match the constituents of an ETF. For more information about ETF universes, see ETF Constituents Selection.

var spy = AddEquity("SPY").Symbol;

diff --git a/01 Cloud Platform/10 Live Trading/03 Data Feeds/09 Brokerage Data Feeds/01 Interactive Brokers/03 Universe Selection.php b/01 Cloud Platform/10 Live Trading/03 Data Feeds/09 Brokerage Data Feeds/01 Interactive Brokers/03 Universe Selection.php

index dd0874de39..ddf39c099d 100644

--- a/01 Cloud Platform/10 Live Trading/03 Data Feeds/09 Brokerage Data Feeds/01 Interactive Brokers/03 Universe Selection.php

+++ b/01 Cloud Platform/10 Live Trading/03 Data Feeds/09 Brokerage Data Feeds/01 Interactive Brokers/03 Universe Selection.php

@@ -1,6 +1,7 @@

-

The universe selection data comes from our Dataset Market, not the TWS market scanners. Universe selection with the IB data feed occurs around 6-7 AM Eastern Time (ET) on Tuesday to Friday and at 2 AM ET on Sunday. Universe selection data isn't available when the IB servers are closed. To check the IB server status, see the Current System Status page on the IB website.

diff --git a/01 Cloud Platform/10 Live Trading/03 Data Feeds/09 Brokerage Data Feeds/03 Tradier/03 Universe Selection.php b/01 Cloud Platform/10 Live Trading/03 Data Feeds/09 Brokerage Data Feeds/03 Tradier/03 Universe Selection.php

index d6e226b0c2..80a91f32b0 100644

--- a/01 Cloud Platform/10 Live Trading/03 Data Feeds/09 Brokerage Data Feeds/03 Tradier/03 Universe Selection.php

+++ b/01 Cloud Platform/10 Live Trading/03 Data Feeds/09 Brokerage Data Feeds/03 Tradier/03 Universe Selection.php

@@ -1,4 +1,5 @@

-

\ No newline at end of file

diff --git a/08 Drafts/03 Writing Algorithms/03 Securities/01 Key Concepts/08 Fundamental Data.html b/03 Writing Algorithms/03 Securities/01 Key Concepts/08 Fundamental Data.html

similarity index 89%

rename from 08 Drafts/03 Writing Algorithms/03 Securities/01 Key Concepts/08 Fundamental Data.html

rename to 03 Writing Algorithms/03 Securities/01 Key Concepts/08 Fundamental Data.html

index 8e2f5c2952..a7c04b7b55 100644

--- a/08 Drafts/03 Writing Algorithms/03 Securities/01 Key Concepts/08 Fundamental Data.html

+++ b/03 Writing Algorithms/03 Securities/01 Key Concepts/08 Fundamental Data.html

@@ -10,4 +10,4 @@

var hasFundamentalData = Securities[_symbol].Fundamentals.HasFundamentalData;

Corporate fundamental data contains all the information on the underlying company of an Equity asset and the information in their financial statements. Since corporate data contains information not found in price and alternative data, adding corporate data to your trading strategies provides you with more information so you can make more informed trading decisions. Corporate fundamental data is available through the US Fundamental Data from Morningstar. To get fundamental data into your algorithm, add a fundamental universe.

+

Corporate fundamental data contains all the information on the underlying company of an Equity asset and the information in their financial statements. Since corporate data contains information not found in price and alternative data, adding corporate data to your trading strategies provides you with more information so you can make more informed trading decisions. Corporate fundamental data is available through the US Fundamental Data from Morningstar.

diff --git a/08 Drafts/03 Writing Algorithms/03 Securities/99 Asset Classes/01 US Equity/06 Corporate Fundamentals/02 Direct Access.php b/03 Writing Algorithms/03 Securities/99 Asset Classes/01 US Equity/06 Corporate Fundamentals/02 Direct Access.php

similarity index 100%

rename from 08 Drafts/03 Writing Algorithms/03 Securities/99 Asset Classes/01 US Equity/06 Corporate Fundamentals/02 Direct Access.php

rename to 03 Writing Algorithms/03 Securities/99 Asset Classes/01 US Equity/06 Corporate Fundamentals/02 Direct Access.php

diff --git a/03 Writing Algorithms/03 Securities/99 Asset Classes/01 US Equity/06 Corporate Fundamentals/02 Properties.php b/03 Writing Algorithms/03 Securities/99 Asset Classes/01 US Equity/06 Corporate Fundamentals/02 Properties.php

deleted file mode 100644

index 38cdf639f0..0000000000

--- a/03 Writing Algorithms/03 Securities/99 Asset Classes/01 US Equity/06 Corporate Fundamentals/02 Properties.php

+++ /dev/null

@@ -1,8 +0,0 @@

-

To get fundamental data, access the FineFundamental properties in your fine universe selection function or access the Fundamentals property of the Equity objects in your fundamental universe.

-

-

-

var fundamentals = Securities[_symbol].Fundamentals;

To get historical fundamental data, set a warm-up period and save the fundamental data during the warm-up period. It’s not currently possible to make a history request for fundamental data in an algorithm. Subscribe to GitHub Issue #4890 to track the feature progress.

\ No newline at end of file

diff --git a/08 Drafts/03 Writing Algorithms/03 Securities/99 Asset Classes/01 US Equity/06 Corporate Fundamentals/03 Universe Selection.html b/03 Writing Algorithms/03 Securities/99 Asset Classes/01 US Equity/06 Corporate Fundamentals/03 Universe Selection.html

similarity index 100%

rename from 08 Drafts/03 Writing Algorithms/03 Securities/99 Asset Classes/01 US Equity/06 Corporate Fundamentals/03 Universe Selection.html

rename to 03 Writing Algorithms/03 Securities/99 Asset Classes/01 US Equity/06 Corporate Fundamentals/03 Universe Selection.html

diff --git a/03 Writing Algorithms/03 Securities/99 Asset Classes/01 US Equity/06 Corporate Fundamentals/04 Data Updates.html b/03 Writing Algorithms/03 Securities/99 Asset Classes/01 US Equity/06 Corporate Fundamentals/04 Data Updates.html

deleted file mode 100644

index dd25a808f1..0000000000

--- a/03 Writing Algorithms/03 Securities/99 Asset Classes/01 US Equity/06 Corporate Fundamentals/04 Data Updates.html

+++ /dev/null

@@ -1 +0,0 @@

-

The US Fundmamental dataset only provides the originally-reported figures. If there was a mistake in reporting a figure, the data value isn't fixed later. In live trading, new fundamental data is available to your algorithms at approximately 6 AM Eastern Time (ET) each day. The majority of the corporate data update occurs once per month, but the financial ratios update daily. If there is no new data for a period of time, the previous data is filled forward.

\ No newline at end of file

diff --git a/08 Drafts/03 Writing Algorithms/03 Securities/99 Asset Classes/01 US Equity/06 Corporate Fundamentals/04 Historical Data.php b/03 Writing Algorithms/03 Securities/99 Asset Classes/01 US Equity/06 Corporate Fundamentals/04 Historical Data.php

similarity index 100%

rename from 08 Drafts/03 Writing Algorithms/03 Securities/99 Asset Classes/01 US Equity/06 Corporate Fundamentals/04 Historical Data.php

rename to 03 Writing Algorithms/03 Securities/99 Asset Classes/01 US Equity/06 Corporate Fundamentals/04 Historical Data.php

diff --git a/08 Drafts/03 Writing Algorithms/03 Securities/99 Asset Classes/01 US Equity/06 Corporate Fundamentals/05 Data Updates.html b/03 Writing Algorithms/03 Securities/99 Asset Classes/01 US Equity/06 Corporate Fundamentals/05 Data Updates.html

similarity index 100%

rename from 08 Drafts/03 Writing Algorithms/03 Securities/99 Asset Classes/01 US Equity/06 Corporate Fundamentals/05 Data Updates.html

rename to 03 Writing Algorithms/03 Securities/99 Asset Classes/01 US Equity/06 Corporate Fundamentals/05 Data Updates.html

diff --git a/08 Drafts/03 Writing Algorithms/03 Securities/99 Asset Classes/01 US Equity/06 Corporate Fundamentals/06 Properties.php b/03 Writing Algorithms/03 Securities/99 Asset Classes/01 US Equity/06 Corporate Fundamentals/06 Properties.php

similarity index 100%

rename from 08 Drafts/03 Writing Algorithms/03 Securities/99 Asset Classes/01 US Equity/06 Corporate Fundamentals/06 Properties.php

rename to 03 Writing Algorithms/03 Securities/99 Asset Classes/01 US Equity/06 Corporate Fundamentals/06 Properties.php

diff --git a/03 Writing Algorithms/12 Universes/01 Key Concepts/05 Selection Functions.html b/03 Writing Algorithms/12 Universes/01 Key Concepts/05 Selection Functions.html

index cb480bd1a7..b660608565 100644

--- a/03 Writing Algorithms/12 Universes/01 Key Concepts/05 Selection Functions.html

+++ b/03 Writing Algorithms/12 Universes/01 Key Concepts/05 Selection Functions.html

@@ -1,27 +1,27 @@

The following example filter function selects the 100 most liquid US Equities.

-

public class MyCoarseUniverseAlgorithm : QCAlgorithm

+

public class MyFundamentalUniverseAlgorithm : QCAlgorithm

{

public override void Initialize()

{

- AddUniverse(CoarseFilterFunction);

+ AddUniverse(FundamentalFilterFunction);

}

- private IEnumerable<Symbol> CoarseFilterFunction(IEnumerable<CoarseFundamental> coarse)

+ private IEnumerable<Symbol> FundamentalFilterFunction(IEnumerable<Fundamental> fundamental)

{

- return (from c in coarse

+ return (from c in fundamental

orderby c.DollarVolume descending

select c.Symbol).Take(100);

}

}

private Universe _universe;

// In Initialize

-_universe = AddUniverse(MyCoarseFilterFunction);

+_universe = AddUniverse(MyFundamentalFilterFunction);

// In OnData

var universeMembers = UniverseManager[_universe.Configuration.Symbol].Members;

@@ -14,12 +14,11 @@

var security = kvp.Value;

}

# In Initialize

-self.universe = self.AddUniverse(self.MyCoarseFilterFunction)

+self.universe = self.AddUniverse(self.MyFundamentalFilterFunction)

# In OnData

universe_members = self.UniverseManager[self.universe.Configuration.Symbol].Members

for kvp in universe_members:

symbol = kvp.Key

- security = kvp.Value

-

+ security = kvp.Value

\ No newline at end of file

diff --git a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/01 Liquidity Universes/01 Introduction.html b/03 Writing Algorithms/12 Universes/03 Equity/01 Liquidity Universes/01 Introduction.html

similarity index 100%

rename from 08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/01 Liquidity Universes/01 Introduction.html

rename to 03 Writing Algorithms/12 Universes/03 Equity/01 Liquidity Universes/01 Introduction.html

diff --git a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/01 Liquidity Universes/02 Create Universes.html b/03 Writing Algorithms/12 Universes/03 Equity/01 Liquidity Universes/02 Create Universes.html

similarity index 100%

rename from 08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/01 Liquidity Universes/02 Create Universes.html

rename to 03 Writing Algorithms/12 Universes/03 Equity/01 Liquidity Universes/02 Create Universes.html

diff --git a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/01 Liquidity Universes/10 Selection Frequency.html b/03 Writing Algorithms/12 Universes/03 Equity/01 Liquidity Universes/10 Selection Frequency.html

similarity index 100%

rename from 08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/01 Liquidity Universes/10 Selection Frequency.html

rename to 03 Writing Algorithms/12 Universes/03 Equity/01 Liquidity Universes/10 Selection Frequency.html

diff --git a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/01 Liquidity Universes/99 Examples.html b/03 Writing Algorithms/12 Universes/03 Equity/01 Liquidity Universes/99 Examples.html

similarity index 100%

rename from 08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/01 Liquidity Universes/99 Examples.html

rename to 03 Writing Algorithms/12 Universes/03 Equity/01 Liquidity Universes/99 Examples.html

diff --git a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/01 Introduction.php b/03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/01 Introduction.php

similarity index 100%

rename from 08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/01 Introduction.php

rename to 03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/01 Introduction.php

diff --git a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/02 Create Universes.php b/03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/02 Create Universes.php

similarity index 99%

rename from 08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/02 Create Universes.php

rename to 03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/02 Create Universes.php

index e7daffea87..8ee3f3cd43 100644

--- a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/02 Create Universes.php

+++ b/03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/02 Create Universes.php

@@ -31,7 +31,7 @@

-

// Take the top 50 by dollar volume using coarse

+

// Take the top 50 by dollar volume using fundamental

// Then the top 10 by PERatio using fine

AddUniverse(

fundamental => (from f in fundamental

diff --git a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/03 Direct Access.php b/03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/03 Direct Access.php

similarity index 100%

rename from 08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/03 Direct Access.php

rename to 03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/03 Direct Access.php

diff --git a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/04 Historical Data.php b/03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/04 Historical Data.php

similarity index 100%

rename from 08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/04 Historical Data.php

rename to 03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/04 Historical Data.php

diff --git a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/10 Selection Frequency.html b/03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/10 Selection Frequency.html

similarity index 100%

rename from 08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/10 Selection Frequency.html

rename to 03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/10 Selection Frequency.html

diff --git a/03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/11 Live Trading Considerations.php b/03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/11 Live Trading Considerations.php

new file mode 100644

index 0000000000..d645576662

--- /dev/null

+++ b/03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/11 Live Trading Considerations.php

@@ -0,0 +1 @@

+

\ No newline at end of file

diff --git a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/99 Examples.html b/03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/99 Examples.html

similarity index 99%

rename from 08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/99 Examples.html

rename to 03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/99 Examples.html

index 7ac7328fb1..54cc9d0bbc 100644

--- a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/99 Examples.html

+++ b/03 Writing Algorithms/12 Universes/03 Equity/02 Fundamental Universes/99 Examples.html

@@ -1,5 +1,5 @@

-

+

The following examples are typical filter functions you may want.

Example 1: Take 500 stocks that are worth more than $10 and have more than $10M daily trading volume

diff --git a/03 Writing Algorithms/12 Universes/03 Equity/03 Dollar Volume Selection.html b/03 Writing Algorithms/12 Universes/03 Equity/03 Dollar Volume Selection.html

deleted file mode 100644

index 31d6407e6a..0000000000

--- a/03 Writing Algorithms/12 Universes/03 Equity/03 Dollar Volume Selection.html

+++ /dev/null

@@ -1,10 +0,0 @@

-

A dollar volume universe enables you pick the most liquid stocks in the market with just one line of code. To add a dollar volume universe, call the Universe.DollarVolume.Top helper method and pass the result to the AddUniverse method.

-

-

-

// Add the 50 stocks with the highest dollar volume

-AddUniverse(Universe.DollarVolume.Top(50));

-

-

// Add the 50 stocks with the highest dollar volume

-self.AddUniverse(self.Universe.DollarVolume.Top(50))

-

-

diff --git a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/03 ETF Constituents Universes/01 Introduction.html b/03 Writing Algorithms/12 Universes/03 Equity/03 ETF Constituents Universes/01 Introduction.html

similarity index 100%

rename from 08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/03 ETF Constituents Universes/01 Introduction.html

rename to 03 Writing Algorithms/12 Universes/03 Equity/03 ETF Constituents Universes/01 Introduction.html

diff --git a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/03 ETF Constituents Universes/02 Create Universes.html b/03 Writing Algorithms/12 Universes/03 Equity/03 ETF Constituents Universes/02 Create Universes.html

similarity index 100%

rename from 08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/03 ETF Constituents Universes/02 Create Universes.html

rename to 03 Writing Algorithms/12 Universes/03 Equity/03 ETF Constituents Universes/02 Create Universes.html

diff --git a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/03 ETF Constituents Universes/10 Selection Frequency.html b/03 Writing Algorithms/12 Universes/03 Equity/03 ETF Constituents Universes/10 Selection Frequency.html

similarity index 100%

rename from 08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/03 ETF Constituents Universes/10 Selection Frequency.html

rename to 03 Writing Algorithms/12 Universes/03 Equity/03 ETF Constituents Universes/10 Selection Frequency.html

diff --git a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/03 ETF Constituents Universes/99 Examples.html b/03 Writing Algorithms/12 Universes/03 Equity/03 ETF Constituents Universes/99 Examples.html

similarity index 100%

rename from 08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/03 ETF Constituents Universes/99 Examples.html

rename to 03 Writing Algorithms/12 Universes/03 Equity/03 ETF Constituents Universes/99 Examples.html

diff --git a/03 Writing Algorithms/12 Universes/03 Equity/03 ETF Constituents Universes/metadata.json b/03 Writing Algorithms/12 Universes/03 Equity/03 ETF Constituents Universes/metadata.json

new file mode 100644

index 0000000000..bd33b20fcd

--- /dev/null

+++ b/03 Writing Algorithms/12 Universes/03 Equity/03 ETF Constituents Universes/metadata.json

@@ -0,0 +1,12 @@

+{

+ "type": "metadata",

+ "values": {

+ "description": "You can select a universe based on the constituents of an ETF, and then you can further filter your universe down with fundamentals.",

+ "keywords": "ETF constituents",

+ "og:description": "You can select a universe based on the constituents of an ETF, and then you can further filter your universe down with fundamentals.",

+ "og:title": "Equity - Documentation QuantConnect.com",

+ "og:type": "website",

+ "og:site_name": "Equity - QuantConnect.com",

+ "og:image": "https://cdn.quantconnect.com/docs/i/writing-algorithms/universes/equity.png"

+ }

+}

diff --git a/03 Writing Algorithms/12 Universes/11 Chained Universes/00 Introduction.html b/03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/00 Introduction.html

similarity index 100%

rename from 03 Writing Algorithms/12 Universes/11 Chained Universes/00 Introduction.html

rename to 03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/00 Introduction.html

diff --git a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/02 Filter Pattern.html b/03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/02 Filter Pattern.html

similarity index 100%

rename from 08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/02 Filter Pattern.html

rename to 03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/02 Filter Pattern.html

diff --git a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/04 Universe Data Weights.html b/03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/04 Universe Data Weights.html

similarity index 100%

rename from 08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/04 Universe Data Weights.html

rename to 03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/04 Universe Data Weights.html

diff --git a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/06 Chain Fundamental and Alternative Data.html b/03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/06 Chain Fundamental and Alternative Data.html

similarity index 100%

rename from 08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/06 Chain Fundamental and Alternative Data.html

rename to 03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/06 Chain Fundamental and Alternative Data.html

diff --git a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/07 Chain ETF and Fundamental.html b/03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/07 Chain ETF and Fundamental.html

similarity index 93%

rename from 08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/07 Chain ETF and Fundamental.html

rename to 03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/07 Chain ETF and Fundamental.html

index a42219c066..1fdaecad6c 100644

--- a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/07 Chain ETF and Fundamental.html

+++ b/03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/07 Chain ETF and Fundamental.html

@@ -2,7 +2,7 @@

- The following example chains a fundamental universe and an ETF constituents universe.

+ The following example chains a fundamental universe and an ETF constituents universe.

It first selects all the constituents of the QQQ ETF and then filters then down to select the 20 assets with the lowest PE ratio.

The output of the fundamental universe selection method is the output of the chained universe.

diff --git a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/08 Chain ETF and Alternative Data.html b/03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/08 Chain ETF and Alternative Data.html

similarity index 94%

rename from 08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/08 Chain ETF and Alternative Data.html

rename to 03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/08 Chain ETF and Alternative Data.html

index cf82999dd5..4deeb5e580 100644

--- a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/08 Chain ETF and Alternative Data.html

+++ b/03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/08 Chain ETF and Alternative Data.html

@@ -1,5 +1,5 @@

diff --git a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/10 Chain ETF and US Equity Options.html b/03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/10 Chain ETF and US Equity Options.html

similarity index 96%

rename from 08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/10 Chain ETF and US Equity Options.html

rename to 03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/10 Chain ETF and US Equity Options.html

index 76bfe4898e..a80d2488b3 100644

--- a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/10 Chain ETF and US Equity Options.html

+++ b/03 Writing Algorithms/12 Universes/03 Equity/04 Chained Universes/10 Chain ETF and US Equity Options.html

@@ -1,5 +1,5 @@

- The following example chains an ETF constituents universe and an Equity Options universe.

+ The following example chains an ETF constituents universe and an Equity Options universe.

It first selects the 30 largest-weighted constituents of QQQ and then selects their call Option contracts that expire within 60 days.

The output of both universes is the output of the chained universe.

An ETF constituents universe lets you select a universe of securities in an ETF. The US ETF Constituents dataset includes 2,650 US ETFs you can use to create your universe. To add an ETF Constituents universe, call the Universe.ETF method.

-

-

-

public class ETFConstituentsAlgorithm : QCAlgorithm

-{

- public override void Initialize()

- {

- AddUniverse(Universe.ETF("SPY", Market.USA, UniverseSettings));

- }

-}

The following table describes the ETF method arguments:

-

-

-

-

-

-

Argument: etfTicker

-

The ETF ticker. To view the supported ETFs in the US ETF Constituents dataset, see Supported ETFs.

-

Data Type: stringstr | Default Value: None

-

-

-

-

-

Argument: market

-

The market of the ETF. If you don't provide an argument, it uses the default Equity market of the brokerage model.

-

Data Type: stringstr | Default Value: None

-

-

-

-

-

Argument: universeSettings

-

The universe settings. If you don't provide an argument, it uses the algorithm UniverseSettings.

-

Data Type: UniverseSettings | Default Value: None

-

-

-

-

-

Argument: universeFilterFunc

-

A function to select some of the ETF constituents for the universe. If you don't provide an argument, it selects all of the constituents.

-

Data Type: Func<IEnumerable<ETFConstituentData>, IEnumerable<Symbol>>Callable[[List[ETFConstituentData]], List[Symbol]] | Default Value: nullNone

-

-

-

-

-

-

To select a subset of the ETF constituents, provide a universeFilterFunc argument. The filter function receives ETFConstituentData objects, which represent one of the ETF constituents. ETFConstituentsData objects have the following attributes:

-

-

-

-

-

-

public class ETFConstituentsAlgorithm : QCAlgorithm

-{

- public override void Initialize()

- {

- var universe = Universe.ETF("SPY", Market.USA, UniverseSettings, ETFConstituentsFilter);

- AddUniverse(universe);

- }

-

- private IEnumerable<Symbol> ETFConstituentsFilter(IEnumerable<ETFConstituentData> constituents)

- {

- // Get the 10 securities with the largest weight in the index

- return constituents.OrderByDescending(c => c.Weight).Take(10).Select(c => c.Symbol);

- }

-}

-

-

class ETFConstituentsAlgorithm(QCAlgorithm):

- def Initialize(self) -> None:

- universe = self.Universe.ETF("SPY", Market.USA, self.UniverseSettings, self.ETFConstituentsFilter)

- self.AddUniverse(universe)

-

- def ETFConstituentsFilter(self, constituents: List[ETFConstituentData]) -> List[Symbol]:

- # Get the 10 securities with the largest weight in the index

- selected = sorted([c for c in constituents if c.Weight],

- key=lambda c: c.Weight, reverse=True)[:10]

- return [c.Symbol for c in selected]

-

diff --git a/03 Writing Algorithms/12 Universes/03 Equity/01 Introduction.html b/03 Writing Algorithms/12 Universes/03 Equity/05 Legacy Fundamental Universes/01 Introduction.html

similarity index 100%

rename from 03 Writing Algorithms/12 Universes/03 Equity/01 Introduction.html

rename to 03 Writing Algorithms/12 Universes/03 Equity/05 Legacy Fundamental Universes/01 Introduction.html

diff --git a/03 Writing Algorithms/12 Universes/03 Equity/02 Coarse Universe Selection.php b/03 Writing Algorithms/12 Universes/03 Equity/05 Legacy Fundamental Universes/02 Coarse Universe Selection.php

similarity index 100%

rename from 03 Writing Algorithms/12 Universes/03 Equity/02 Coarse Universe Selection.php

rename to 03 Writing Algorithms/12 Universes/03 Equity/05 Legacy Fundamental Universes/02 Coarse Universe Selection.php

diff --git a/03 Writing Algorithms/12 Universes/03 Equity/05 Fundamentals Selection.php b/03 Writing Algorithms/12 Universes/03 Equity/05 Legacy Fundamental Universes/05 Fundamentals Selection.php

similarity index 89%

rename from 03 Writing Algorithms/12 Universes/03 Equity/05 Fundamentals Selection.php

rename to 03 Writing Algorithms/12 Universes/03 Equity/05 Legacy Fundamental Universes/05 Fundamentals Selection.php

index a77ceb73ab..aa51050353 100644

--- a/03 Writing Algorithms/12 Universes/03 Equity/05 Fundamentals Selection.php

+++ b/03 Writing Algorithms/12 Universes/03 Equity/05 Legacy Fundamental Universes/05 Fundamentals Selection.php

@@ -47,7 +47,7 @@

QuantConnect Coarse and Fine Universe Selection

-

To add a fundamental universe, in the Initialize method, pass two filter functions to the AddUniverse method. The first filter function can be a coarse universe filter, dollar volume filter, or an ETF constituents filter. The second filter function receives a list of FineFundamental objects and must return a list of Symbol objects. The list of FineFundamental objects contains a subset of the Symbol objects that the first filter function returned. The Symbol objects you return from the second function are the constituents of the fundamental universe and LEAN automatically creates subscriptions for them. Don't call AddEquity in the filter function.

+

To add a fundamental universe, in the Initialize method, pass two filter functions to the AddUniverse method. The first filter function can be a coarse universe filter, dollar volume filter, or an ETF constituents filter. The second filter function receives a list of FineFundamental objects and must return a list of Symbol objects. The list of FineFundamental objects contains a subset of the Symbol objects that the first filter function returned. The Symbol objects you return from the second function are the constituents of the fundamental universe and LEAN automatically creates subscriptions for them. Don't call AddEquity in the filter function.

Tip:

diff --git a/03 Writing Algorithms/12 Universes/03 Equity/05 Legacy Fundamental Universes/07 Live Trading Considerations.php b/03 Writing Algorithms/12 Universes/03 Equity/05 Legacy Fundamental Universes/07 Live Trading Considerations.php

new file mode 100644

index 0000000000..d645576662

--- /dev/null

+++ b/03 Writing Algorithms/12 Universes/03 Equity/05 Legacy Fundamental Universes/07 Live Trading Considerations.php

@@ -0,0 +1 @@

+

\ No newline at end of file

diff --git a/03 Writing Algorithms/12 Universes/03 Equity/08 Examples.html b/03 Writing Algorithms/12 Universes/03 Equity/05 Legacy Fundamental Universes/08 Examples.html

similarity index 100%

rename from 03 Writing Algorithms/12 Universes/03 Equity/08 Examples.html

rename to 03 Writing Algorithms/12 Universes/03 Equity/05 Legacy Fundamental Universes/08 Examples.html

diff --git a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/06 Alternative Data Universes/01 Introduction.html b/03 Writing Algorithms/12 Universes/03 Equity/06 Alternative Data Universes/01 Introduction.html

similarity index 100%

rename from 08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/06 Alternative Data Universes/01 Introduction.html

rename to 03 Writing Algorithms/12 Universes/03 Equity/06 Alternative Data Universes/01 Introduction.html

diff --git a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/06 Alternative Data Universes/02 Supported Datasets.html b/03 Writing Algorithms/12 Universes/03 Equity/06 Alternative Data Universes/02 Supported Datasets.html

similarity index 100%

rename from 08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/06 Alternative Data Universes/02 Supported Datasets.html

rename to 03 Writing Algorithms/12 Universes/03 Equity/06 Alternative Data Universes/02 Supported Datasets.html

diff --git a/03 Writing Algorithms/12 Universes/03 Equity/06 Selection Frequency.html b/03 Writing Algorithms/12 Universes/03 Equity/06 Selection Frequency.html

deleted file mode 100644

index fbb9bc72ad..0000000000

--- a/03 Writing Algorithms/12 Universes/03 Equity/06 Selection Frequency.html

+++ /dev/null

@@ -1 +0,0 @@

-

Equity universes run on a daily basis.

diff --git a/03 Writing Algorithms/12 Universes/03 Equity/07 Live Trading Considerations.php b/03 Writing Algorithms/12 Universes/03 Equity/07 Live Trading Considerations.php

deleted file mode 100644

index 72a971d5d3..0000000000

--- a/03 Writing Algorithms/12 Universes/03 Equity/07 Live Trading Considerations.php

+++ /dev/null

@@ -1 +0,0 @@

-

diff --git a/03 Writing Algorithms/12 Universes/03 Equity/metadata.json b/03 Writing Algorithms/12 Universes/03 Equity/metadata.json

deleted file mode 100644

index 3e962bd65c..0000000000

--- a/03 Writing Algorithms/12 Universes/03 Equity/metadata.json

+++ /dev/null

@@ -1,12 +0,0 @@

-{

- "type": "metadata",

- "values": {

- "description": "You can select a universe based on coarse data or the constituents of an ETF, and then you can further filter your universe down with fundamentals.",

- "keywords": "Coarse Fundamental, fine fundamental, etf constituents, fundamental data",

- "og:description": "You can select a universe based on coarse data or the constituents of an ETF, and then you can further filter your universe down with fundamentals.",

- "og:title": "Equity - Documentation QuantConnect.com",

- "og:type": "website",

- "og:site_name": "Equity - QuantConnect.com",

- "og:image": "https://cdn.quantconnect.com/docs/i/writing-algorithms/universes/equity.png"

- }

-}

diff --git a/08 Drafts/03 Writing Algorithms/12 Universes/05 Crypto/03 Alternative Data Universes.html b/03 Writing Algorithms/12 Universes/05 Crypto/03 Alternative Data Universes.html

similarity index 100%

rename from 08 Drafts/03 Writing Algorithms/12 Universes/05 Crypto/03 Alternative Data Universes.html

rename to 03 Writing Algorithms/12 Universes/05 Crypto/03 Alternative Data Universes.html

diff --git a/03 Writing Algorithms/12 Universes/11 Chained Universes/02 Filter Pattern.html b/03 Writing Algorithms/12 Universes/11 Chained Universes/02 Filter Pattern.html

deleted file mode 100644

index d1d01ce744..0000000000

--- a/03 Writing Algorithms/12 Universes/11 Chained Universes/02 Filter Pattern.html

+++ /dev/null

@@ -1,5 +0,0 @@

-

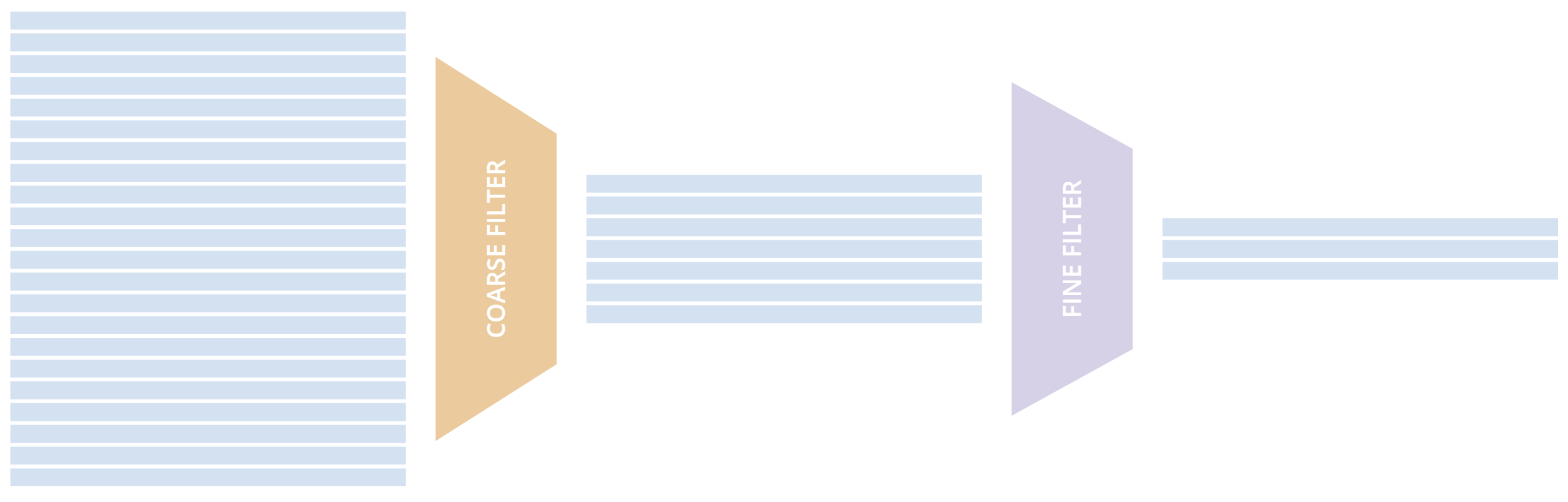

- Universes filter a large set of Symbol objects by a coarse filter to quickly reduce the data processing requirement. This is often a first step before applying a second filter or requesting alternative data. For example, a strategy might only be interested in easily tradable liquid assets so quickly eliminates all stocks with less than $1M USD / day in trading volume.

-

-

-

The order of your filters can improve the speed of your research. By applying filters that narrow the universe the most, or are the lightest weight first, you can significantly reduce the amount of data your algorithm processes. Unless necessary, you can also not return any selections from earlier filters to further improve research speed, keeping only the universe data for later filters.

\ No newline at end of file

diff --git a/03 Writing Algorithms/12 Universes/11 Chained Universes/04 Universe Data Weights.html b/03 Writing Algorithms/12 Universes/11 Chained Universes/04 Universe Data Weights.html

deleted file mode 100644

index 8171a5c8aa..0000000000

--- a/03 Writing Algorithms/12 Universes/11 Chained Universes/04 Universe Data Weights.html

+++ /dev/null

@@ -1,21 +0,0 @@

-

- To speed up your algorithm, request the lightest weight data first before chaining heavier filters or adding alternative data. The following table shows the size each dataset:

Universes typically run overnight and are available before market open. Universes are not currently "ordered", so universe chaining works best with slower universes. For example, use a slow-changing ETF Constituents Universe to set the Symbol list for alternative data.

\ No newline at end of file

diff --git a/03 Writing Algorithms/12 Universes/11 Chained Universes/06 Chaining Coarse and Alternative Data.html b/03 Writing Algorithms/12 Universes/11 Chained Universes/06 Chaining Coarse and Alternative Data.html

deleted file mode 100644

index f70decf701..0000000000

--- a/03 Writing Algorithms/12 Universes/11 Chained Universes/06 Chaining Coarse and Alternative Data.html

+++ /dev/null

@@ -1,99 +0,0 @@

-

-The following example chains the QuiverQuantTwitterFollowersUniverse alternative universe to the coarse universe. It first selects the 100 most liquid US Equities and then filters them down based on their Twitter followers number and weekly change. The output of the alternative universe selection method is the output of the chained universe.

-

from AlgorithmImports import *

-

-class ChainedUniverseAlgorithm(QCAlgorithm):

-

- coarse = []

- universe_coarse = None

- universe_twitter = None

-

- def Initialize(self):

- self.SetCash(100000)

- self.SetStartDate(2023, 1, 2)

- self.universe_coarse = self.AddUniverse(self.CoarseFilterFunction)

- self.universe_twitter = self.AddUniverse(QuiverQuantTwitterFollowersUniverse, "QuiverQuantTwitterFollowersUniverse", Resolution.Daily, self.FollowerSelection)

-

- def CoarseFilterFunction(self, coarse: List[CoarseFundamental]) -> List[Symbol]:

- sorted_by_dollar_volume = sorted(coarse, key=lambda x: x.DollarVolume, reverse=True)

- self.coarse = [c.Symbol for c in sorted_by_dollar_volume[:100]]

- return Universe.Unchanged

-

- def FollowerSelection(self, alt_coarse: List[QuiverQuantTwitterFollowersUniverse]) -> List[Symbol]:

- self.followers = [d.Symbol for d in alt_coarse if d.Followers > 200000 and d.WeekPercentChange > 0]

- return list(set(self.coarse) & set(self.followers))

-

- def OnSecuritiesChanged(self, changes):

- for added in changes.AddedSecurities:

- self.AddData(QuiverQuantTwitterFollowers, added.Symbol)

-

- def OnData(self, data):

- # Prices in the slice from the universe selection

- # Alternative data in slice from OnSecuritiesChanged Addition

- # for ticker,bar in data.Bars.items():

- # pass

- for dataset_symbol, data_point in data.Get(QuiverQuantTwitterFollowers).items():

- self.Debug(f"{dataset_symbol} followers at {data.Time}: {data_point.Followers}")

-

diff --git a/03 Writing Algorithms/12 Universes/11 Chained Universes/08 Chaining ETF Universe and Alt Data.html b/03 Writing Algorithms/12 Universes/11 Chained Universes/08 Chaining ETF Universe and Alt Data.html

deleted file mode 100644

index dd50b89d13..0000000000

--- a/03 Writing Algorithms/12 Universes/11 Chained Universes/08 Chaining ETF Universe and Alt Data.html

+++ /dev/null

@@ -1,104 +0,0 @@

-

-The following example chains a QuiverQuantTwitterFollowersUniverse alternative universe to the SPY ETF universe. It first selects all constituents of SPY and then filters them down with based on their Twitter followers number and weekly change. The output of the alternative universe selection method is the output of the chained universe.

-

from AlgorithmImports import *

-

-class ChainedUniverseAlgorithm(QCAlgorithm):

-

- etf = []

- universe_etf = None

- universe_twitter = None

-

- def Initialize(self):

- self.SetCash(100000)

- self.SetStartDate(2023, 1, 2)

-

- self.universe_etf = self.AddUniverse(self.Universe.ETF("SPY", Market.USA, self.UniverseSettings, self.ETFConstituentsFilter))

- # or symbol = Symbol.Create("SPY", SecurityType.Equity, Market.USA)

- # self.universe_etf = self.AddUniverseSelection(ETFConstituentsUniverseSelectionModel(

- # symbol, self.UniverseSettings, self.ETFConstituentsFilter))

- self.universe_twitter = self.AddUniverse(QuiverQuantTwitterFollowersUniverse,

- "QuiverQuantTwitterFollowersUniverse", Resolution.Daily, self.FollowerSelection)

-

- def ETFConstituentsFilter(self, constituents: List[ETFConstituentData]) -> List[Symbol]:

- self.etf = [c.Symbol for c in constituents]

- return Universe.Unchanged

-

- def FollowerSelection(self, alt_coarse: List[QuiverQuantTwitterFollowersUniverse]) -> List[Symbol]:

- self.followers = [d.Symbol for d in alt_coarse if d.Followers > 200000 and d.WeekPercentChange > 0]

- return list(set(self.etf) & set(self.followers))

-

- def OnSecuritiesChanged(self, changes):

- for added in changes.AddedSecurities:

- self.AddData(QuiverQuantTwitterFollowers, added.Symbol)

-

- def OnData(self, data):

- # Prices in the slice from the universe selection

- # Alternative data in slice from OnSecuritiesChanged Addition

- # for ticker,bar in data.Bars.items():

- # pass

- for dataset_symbol, data_point in data.Get(QuiverQuantTwitterFollowers).items():

- self.Debug(f"{dataset_symbol} followers at {data.Time}: {data_point.Followers}")

-

\ No newline at end of file

diff --git a/03 Writing Algorithms/12 Universes/11 Chained Universes/10 Chaining to US Equity Options.html b/03 Writing Algorithms/12 Universes/11 Chained Universes/10 Chaining to US Equity Options.html

deleted file mode 100644

index d18b345ac9..0000000000

--- a/03 Writing Algorithms/12 Universes/11 Chained Universes/10 Chaining to US Equity Options.html

+++ /dev/null

@@ -1,108 +0,0 @@

-

The following example chains an OptionFilterUniverse to the QQQ ETF universe. It first selects the 30 largest-weighted constituents of QQQ and then selects their call Option contracts that expire within 60 days.

from AlgorithmImports import *

-

-class ChainedUniverseAlgorithm(QCAlgorithm):

-

- universe_etf = None

- universe_fine = None

-

- def Initialize(self):

- self.SetCash(100000)

- self.SetStartDate(2023, 2, 2)

-

- self.universe_etf = self.Universe.ETF("QQQ", Market.USA, self.UniverseSettings, self.ETFConstituentsFilter)

- self.universe_fine = self.AddUniverse(self.universe_etf, self.FineSelection)

-

- def ETFConstituentsFilter(self, constituents: List[ETFConstituentData]) -> List[Symbol]:

- return [c.Symbol for c in constituents]

-

- def FineSelection(self, fine: List[FineFundamental]) -> List[Symbol]:

- sorted_by_pe_ratio = sorted(fine, key=lambda f: f.ValuationRatios.PERatio)

- return [f.Symbol for f in sorted_by_pe_ratio[:20]]

-

- def OnData(self, data):

- for symbol in data.Keys:

- self.Debug(f"{symbol} PE Ratio: {self.Securities[symbol].Fundamentals.ValuationRatios.PERatio}")

-

diff --git a/03 Writing Algorithms/12 Universes/12 Alternative Data Universes/01 Introduction.html b/03 Writing Algorithms/12 Universes/12 Alternative Data Universes/01 Introduction.html

deleted file mode 100644

index a25845514d..0000000000

--- a/03 Writing Algorithms/12 Universes/12 Alternative Data Universes/01 Introduction.html

+++ /dev/null

@@ -1 +0,0 @@

-

An alternative data universe lets you select a basket of assets based on an alternative dataset that's linked to securities. If you use an alternative data universe, you limit your universe to only the securities in the dataset, which avoids unnecessary subscriptions.

\ No newline at end of file

diff --git a/03 Writing Algorithms/12 Universes/12 Alternative Data Universes/02 Supported Datasets.php b/03 Writing Algorithms/12 Universes/12 Alternative Data Universes/02 Supported Datasets.php

deleted file mode 100644

index 5d774e89c5..0000000000

--- a/03 Writing Algorithms/12 Universes/12 Alternative Data Universes/02 Supported Datasets.php

+++ /dev/null

@@ -1,3 +0,0 @@

-

\ No newline at end of file

diff --git a/03 Writing Algorithms/12 Universes/12 Alternative Data Universes/metadata.json b/03 Writing Algorithms/12 Universes/12 Alternative Data Universes/metadata.json

deleted file mode 100644

index 4128927f28..0000000000

--- a/03 Writing Algorithms/12 Universes/12 Alternative Data Universes/metadata.json

+++ /dev/null

@@ -1,12 +0,0 @@

-{

- "type": "metadata",

- "values": {

- "description": "An alternative data universe lets you select a basket of assets based on an alternative dataset that's linked to securities.",

- "keywords": "universe selection, alternative data, alt data",

- "og:description": "An alternative data universe lets you select a basket of assets based on an alternative dataset that's linked to securities.",

- "og:title": "Alternative Data Universes - Documentation QuantConnect.com",

- "og:type": "website",

- "og:site_name": "Alternative Data Universes - QuantConnect.com",

- "og:image": "https://cdn.quantconnect.com/docs/i/writing-algorithms/universes/alternative-data-universes.png"

- }

-}

diff --git a/03 Writing Algorithms/16 Importing Data/03 Bulk Downloads/05 Transport Binary Data.html b/03 Writing Algorithms/16 Importing Data/03 Bulk Downloads/05 Transport Binary Data.html

index 35f8f7c405..34074d0a94 100644

--- a/03 Writing Algorithms/16 Importing Data/03 Bulk Downloads/05 Transport Binary Data.html

+++ b/03 Writing Algorithms/16 Importing Data/03 Bulk Downloads/05 Transport Binary Data.html

@@ -13,7 +13,7 @@

base64_str = base64.b64encode(pickle_bytes).decode('ascii')

You need to use a SymbolData class instead of assigning the indicators to the CoarseFundamental object because you can't create custom propertiesattributes on CoarseFundamental objects like you can with Security objects.

+

You need to use a SymbolData class instead of assigning the indicators to the Fundamental object because you can't create custom propertiesattributes on Fundamental objects like you can with Security objects.

diff --git a/03 Writing Algorithms/28 Indicators/08 Indicator Universes/03 Define the Universe.html b/03 Writing Algorithms/28 Indicators/08 Indicator Universes/03 Define the Universe.html

index 1930f2c49a..acdeb95c89 100644

--- a/03 Writing Algorithms/28 Indicators/08 Indicator Universes/03 Define the Universe.html

+++ b/03 Writing Algorithms/28 Indicators/08 Indicator Universes/03 Define the Universe.html

@@ -15,25 +15,25 @@

self.UniverseSettings.Resolution = Resolution.Daily

self.UniverseSettings.Leverage = 2

- self.coarse_count = 10

+ self.count = 10

self.averages = { }

# this add universe method accepts two parameters:

- # - coarse selection function: accepts an IEnumerable<CoarseFundamental> and returns an IEnumerable<Symbol>

- self.AddUniverse(self.CoarseSelectionFunction)

+ # - fundamental selection function: accepts an IEnumerable<Fundamental> and returns an IEnumerable<Symbol>

+ self.AddUniverse(self.FundamentalSelectionFunction)

# sort the data by daily dollar volume and take the top 'NumberOfSymbols'

- def CoarseSelectionFunction(self, coarse: List[CoarseFundamental]) -> List[Symbol]:

+ def FundamentalSelectionFunction(self, fundamental: List[Fundamental]) -> List[Symbol]:

# We are going to use a dictionary to refer the object that will keep the moving averages

- for cf in coarse:

- if cf.Symbol not in self.averages:

- self.averages[cf.Symbol] = SymbolData(cf.Symbol)

+ for f in fundamental:

+ if f.Symbol not in self.averages:

+ self.averages[f.Symbol] = SymbolData(f.Symbol)

# Updates the SymbolData object with current EOD price

- avg = self.averages[cf.Symbol]

- avg.update(cf.EndTime, cf.AdjustedPrice)

+ avg = self.averages[f.Symbol]

+ avg.update(f.EndTime, f.AdjustedPrice)

# Filter the values of the dict: we only want up-trending securities

values = list(filter(lambda x: x.is_uptrend, self.averages.values()))

@@ -41,11 +41,11 @@

# Sorts the values of the dict: we want those with greater difference between the moving averages

values.sort(key=lambda x: x.scale, reverse=True)

- for x in values[:self.coarse_count]:

+ for x in values[:self.count]:

self.Log('symbol: ' + str(x.symbol.Value) + ' scale: ' + str(x.scale))

# we need to return only the symbol objects

- return [ x.symbol for x in values[:self.coarse_count] ]

+ return [ x.symbol for x in values[:self.count] ]

namespace QuantConnect.Algorithm.CSharp

{

public class EmaCrossUniverseSelectionAlgorithm : QCAlgorithm

@@ -56,7 +56,7 @@

// use Buffer+Count to leave a little in cash

private const decimal TargetPercent = 0.1m;

private SecurityChanges _changes = SecurityChanges.None;

- // holds our coarse fundamental indicators by symbol

+ // holds our fundamental indicators by symbol

private readonly ConcurrentDictionary<Symbol, SelectionData> _averages = new ConcurrentDictionary<Symbol, SelectionData>();

public override void Initialize()

@@ -68,19 +68,19 @@

SetEndDate(2015, 01, 01);

SetCash(100*1000);

- AddUniverse(coarse =>

+ AddUniverse(fundamental =>

{

- return (from cf in coarse

+ return (from f in fundamental

// grab th SelectionData instance for this symbol

- let avg = _averages.GetOrAdd(cf.Symbol, sym => new SelectionData())

+ let avg = _averages.GetOrAdd(f.Symbol, sym => new SelectionData())

// Update returns true when the indicators are ready, so don't accept until they are

- where avg.Update(cf.EndTime, cf.AdjustedPrice)

+ where avg.Update(f.EndTime, f.AdjustedPrice)

// only pick symbols who have their 50 day ema over their 100 day ema

where avg.Fast > avg.Slow*(1 + Tolerance)

// prefer symbols with a larger delta by percentage between the two averages

orderby avg.ScaledDelta descending

// we only need to return the symbol and return 'Count' symbols

- select cf.Symbol).Take(Count);

+ select f.Symbol).Take(Count);

});

}

}

diff --git a/03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/01 Key Concepts/04 Multi-Universe Algorithms.html b/03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/01 Key Concepts/04 Multi-Universe Algorithms.html

index 0fd318ac6c..54a81e92b5 100644

--- a/03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/01 Key Concepts/04 Multi-Universe Algorithms.html

+++ b/03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/01 Key Concepts/04 Multi-Universe Algorithms.html

@@ -1,11 +1,14 @@

You can add multiple Universe Selection models to a single algorithm.

A FundamentalUniverseSelectionModel selects a universe of US Equities based on CoarseFundamental and, sometimes, FineFundamental data. If the model uses CoarseFundamental data, it relies on the US Equity Coarse Universe dataset. If the Universe Selection model uses FineFundamental data, it relies on the US Fundamental dataset.

+

A FundamentalUniverseSelectionModel selects a universe of US Equities based on Fundamental data. Depending on the Fundamental properties you use, these universes rely on the US Equity Coarse Universe dataset, the US Fundamental dataset, or both.

These types of universes operate on daily schedule. In backtests, they select assets at midnight. In live trading, the selection timing depends on the data feed you use.

-

If you use a fundamental Universe Selection model, the only way to unsubscribe from a security is to return a list from the selection functions that doesn't include the security Symbol. The RemoveSecurity method doesn't work with these types of Universe Selection models.

-

+

If you use a fundamental Universe Selection model, the only way to unsubscribe from a security is to return a list from the selection function that doesn't include the security Symbol. The RemoveSecurity method doesn't work with these types of Universe Selection models.

diff --git a/08 Drafts/03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/04 Fundamental Universes/02 Fundamental Selection.html b/03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/04 Fundamental Universes/02 Fundamental Selection.html

similarity index 100%

rename from 08 Drafts/03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/04 Fundamental Universes/02 Fundamental Selection.html

rename to 03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/04 Fundamental Universes/02 Fundamental Selection.html

diff --git a/08 Drafts/03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/04 Fundamental Universes/03 EMA Cross Selection.html b/03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/04 Fundamental Universes/03 EMA Cross Selection.html

similarity index 100%

rename from 08 Drafts/03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/04 Fundamental Universes/03 EMA Cross Selection.html

rename to 03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/04 Fundamental Universes/03 EMA Cross Selection.html

diff --git a/03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/04 Fundamental Universes/15 EMA Cross Selection.html b/03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/04 Fundamental Universes/15 EMA Cross Selection.html

deleted file mode 100644

index 9e95a2585a..0000000000

--- a/03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/04 Fundamental Universes/15 EMA Cross Selection.html

+++ /dev/null

@@ -1,54 +0,0 @@

-

The EmaCrossUniverseSelectionModel applies two exponential moving average (EMA) indicators to the price history of assets and then selects the assets that have their fast EMA furthest above their slow EMA on a percentage basis.

-

-

-

public override void Initialize()

-{

- AddUniverseSelection(new EmaCrossUniverseSelectionModel());

-}

diff --git a/08 Drafts/03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/04 Fundamental Universes/99 Examples.html b/03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/04 Fundamental Universes/99 Examples.html

similarity index 100%

rename from 08 Drafts/03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/04 Fundamental Universes/99 Examples.html

rename to 03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/04 Fundamental Universes/99 Examples.html

diff --git a/03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/04 Fundamental Universes/metadata.json b/03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/04 Fundamental Universes/metadata.json

index c657d0bb02..68844a3476 100644

--- a/03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/04 Fundamental Universes/metadata.json

+++ b/03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/04 Fundamental Universes/metadata.json

@@ -1,9 +1,9 @@

{

"type": "metadata",

"values": {

- "description": "A FundamentalUniverseSelectionModel selects a universe of US Equities based on CoarseFundamental and, sometimes, FineFundamental data.",

- "keywords": "US Equity universe, operate on daily schedule, fundamental Universe Selection model, coarse selection function, ine selection function, provides corporate fundamental data, ema cross universe selection, uncorrelated asset selection",

- "og:description": "A FundamentalUniverseSelectionModel selects a universe of US Equities based on CoarseFundamental and, sometimes, FineFundamental data.",

+ "description": "A FundamentalUniverseSelectionModel selects a universe of US Equities based on Fundamental data.",

+ "keywords": "US Equity universe, operate on daily schedule, fundamental Universe Selection model, fundamental selection function, provides corporate fundamental data, ema cross universe selection, uncorrelated asset selection",

+ "og:description": "A FundamentalUniverseSelectionModel selects a universe of US Equities based on Fundamental data.",

"og:title": "Fundamental Universes - Documentation QuantConnect.com",

"og:type": "website",

"og:site_name": "Fundamental Universes - QuantConnect.com",

diff --git a/08 Drafts/03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/09 Legacy Fundamental Universes/01 Introduction.html b/03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/09 Legacy Fundamental Universes/01 Introduction.html

similarity index 100%

rename from 08 Drafts/03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/09 Legacy Fundamental Universes/01 Introduction.html

rename to 03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/09 Legacy Fundamental Universes/01 Introduction.html

diff --git a/03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/04 Fundamental Universes/13 Coarse Fundamental Selection.html b/03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/09 Legacy Fundamental Universes/13 Coarse Fundamental Selection.html

similarity index 100%

rename from 03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/04 Fundamental Universes/13 Coarse Fundamental Selection.html

rename to 03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/09 Legacy Fundamental Universes/13 Coarse Fundamental Selection.html

diff --git a/03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/04 Fundamental Universes/14 Fine Fundamental Selection.html b/03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/09 Legacy Fundamental Universes/14 Fine Fundamental Selection.html

similarity index 100%

rename from 03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/04 Fundamental Universes/14 Fine Fundamental Selection.html

rename to 03 Writing Algorithms/34 Algorithm Framework/02 Universe Selection/09 Legacy Fundamental Universes/14 Fine Fundamental Selection.html

diff --git a/03 Writing Algorithms/34 Algorithm Framework/05 Risk Management/02 Supported Models/06 Maximum Sector Exposure Model.html b/03 Writing Algorithms/34 Algorithm Framework/05 Risk Management/02 Supported Models/06 Maximum Sector Exposure Model.html

index ff234475a7..07a41c9505 100644

--- a/03 Writing Algorithms/34 Algorithm Framework/05 Risk Management/02 Supported Models/06 Maximum Sector Exposure Model.html

+++ b/03 Writing Algorithms/34 Algorithm Framework/05 Risk Management/02 Supported Models/06 Maximum Sector Exposure Model.html

@@ -1,4 +1,4 @@

-

The MaximumSectorExposureRiskManagementModel limits the absolute portfolio exposure in a each industry sector to a predefined maximum percentage. If the absolute portfolio exposure exceeds the maximum percentage, the weight of each Equity in the sector is scaled down so the sector doesn't exceed the maximum percentage. This process requires assets that are selected by Morningstar fine fundamental data. This model can operate even when the Portfolio Construction model provides an empty list of PortfolioTarget objects.

+

The MaximumSectorExposureRiskManagementModel limits the absolute portfolio exposure in a each industry sector to a predefined maximum percentage. If the absolute portfolio exposure exceeds the maximum percentage, the weight of each Equity in the sector is scaled down so the sector doesn't exceed the maximum percentage. This process requires assets that are selected by Morningstar fundamental data. This model can operate even when the Portfolio Construction model provides an empty list of PortfolioTarget objects.

\ No newline at end of file

diff --git a/03 Writing Algorithms/40 Live Trading/99 Signal Exports/03 Numerai/04 Universe Selection.html b/03 Writing Algorithms/40 Live Trading/99 Signal Exports/03 Numerai/04 Universe Selection.html

index bc591c8fe3..834d2d044b 100644

--- a/03 Writing Algorithms/40 Live Trading/99 Signal Exports/03 Numerai/04 Universe Selection.html

+++ b/03 Writing Algorithms/40 Live Trading/99 Signal Exports/03 Numerai/04 Universe Selection.html

@@ -1,6 +1,6 @@

The Numerai Signals stock market universe covers roughly the top 5,000 largest stocks in the world. The universe available on QuantConnect that's the closest match to the Numerai Signals universe is the CRSP US Total Market Index, which represents approximately 100% of the investable US Equity market regularly traded on the New York Stock Exchange and Nasdaq. This Index doesn't contain all of the stocks in the Numerai Signals universe, but you don't need to submit signals for all the stocks in the Numerai Signals universe.

-

To get the constituents of the CRSP US Total Market Index, add an ETF constituents universe for the Vanguard Total Stock Market ETF, VTI.

+

To get the constituents of the CRSP US Total Market Index, add an ETF constituents universe for the Vanguard Total Stock Market ETF, VTI.

_etfSymbol = AddEquity("VTI").Symbol;

diff --git a/04 Research Environment/03 Datasets/06 Equity Fundamental Data/01 Introduction.html b/04 Research Environment/03 Datasets/06 Equity Fundamental Data/01 Introduction.html

index 1e9b27e6fb..b75cc094ed 100644

--- a/04 Research Environment/03 Datasets/06 Equity Fundamental Data/01 Introduction.html

+++ b/04 Research Environment/03 Datasets/06 Equity Fundamental Data/01 Introduction.html

@@ -1 +1 @@

-

This page explains how to request, manipulate, and visualize historical Equity Fundamental data. Corporate fundamental data is available through the US Fundamental Data from Morningstar.

\ No newline at end of file

+

This page explains how to request, manipulate, and visualize historical Equity Fundamental data. Corporate fundamental data is available through the US Fundamental Data from Morningstar.

diff --git a/08 Drafts/04 Research Environment/03 Datasets/06 Equity Fundamental Data/02 Create Subscriptions.php b/04 Research Environment/03 Datasets/06 Equity Fundamental Data/02 Create Subscriptions.php

similarity index 100%

rename from 08 Drafts/04 Research Environment/03 Datasets/06 Equity Fundamental Data/02 Create Subscriptions.php

rename to 04 Research Environment/03 Datasets/06 Equity Fundamental Data/02 Create Subscriptions.php

diff --git a/04 Research Environment/03 Datasets/06 Equity Fundamental Data/03 Create Subscriptions.php b/04 Research Environment/03 Datasets/06 Equity Fundamental Data/03 Create Subscriptions.php

deleted file mode 100644

index 03c15fd967..0000000000

--- a/04 Research Environment/03 Datasets/06 Equity Fundamental Data/03 Create Subscriptions.php

+++ /dev/null

@@ -1,41 +0,0 @@

-

Follow these steps to subscribe to an Equity security:

-

-

-

-

Create a QuantBook.

-

-

var qb = new QuantBook();

-

qb = QuantBook()

-

-

Call the AddEquity method with a ticker and then save a reference to the Equity Symbol.

-

-

-

var symbols = new []

- {

- "AAL", // American Airlines Group, Inc.

- "ALGT", // Allegiant Travel Company

- "ALK", // Alaska Air Group, Inc.

- "DAL", // Delta Air Lines, Inc.

- "LUV", // Southwest Airlines Company

- "SKYW", // SkyWest, Inc.

- "UAL" // United Air Lines

- }

- .Select(ticker => qb.AddEquity(ticker).Symbol);

-

symbols = [qb.AddEquity(ticker).Symbol

- for ticker in [

- "AAL", # American Airlines Group, Inc.

- "ALGT", # Allegiant Travel Company

- "ALK", # Alaska Air Group, Inc.

- "DAL", # Delta Air Lines, Inc.

- "LUV", # Southwest Airlines Company

- "SKYW", # SkyWest, Inc.

- "UAL" # United Air Lines

- ]]

-

-

-

-

-

To view the supported assets in the US Equities dataset, see the Data Explorer.

\ No newline at end of file

diff --git a/04 Research Environment/03 Datasets/06 Equity Fundamental Data/04 Get Historical Data.html b/04 Research Environment/03 Datasets/06 Equity Fundamental Data/04 Get Historical Data.html

index 73e7e4f33b..9ccb04880d 100644

--- a/04 Research Environment/03 Datasets/06 Equity Fundamental Data/04 Get Historical Data.html

+++ b/04 Research Environment/03 Datasets/06 Equity Fundamental Data/04 Get Historical Data.html

@@ -1,14 +1,112 @@

-

You need a subscription before you can request historical fundamental data for a US Equity.

+

+ You need a subscription before you can request historical fundamental data for US Equities.

+ On the time dimension, you can request an amount of historical data based on a trailing number of bars, a trailing period of time, or a defined period of time.

+ On the security dimension, you can request historical data for a single US Equity, a set of US Equities, or all of the US Equities in the US Fundamental dataset.

+ On the property dimension, you can call the History method to get all fundamental properties or you can call the GetFundamental method to get a specific property (for example, the price–earnings ratio).

+

-

To get historical data, call the GetFundamental method with a list of Symbol objects, a fundamental data field name, a start DateTimedatetime, and an end DateTimedatetime. The start and end times you provide are based in the notebook time zone. To view the possible fundamental data field names, see the FineFundamental attributes in Data Point Attributes. For example, to get data for airline companies over 2014, run:

+

+ When you call the History method, you can request Fundamental or Fundamentals objects.

+ If you use Fundamental, the method returns all fundamental properties for the Symbol object(s) you provide.

+ If you use Fundamentals, the method returns all fundamental properties for all the US Equities in the US Fundamental dataset that were trading during that time period you request, including companies that no longer trade.

+

+

Trailing Number of Trading Days

+

To get historical data for a number of trailing trading days, call the History method with the number of trading days. If you didn't use Resolution.Daily when you subscribed to the US Equities, pass it as the last argument to the History method.

-

var startTime = new DateTime(2014, 1, 1);

-var endTime = new DateTime(2015, 1, 1);

-var history = qb.GetFundamental(symbols, "ValuationRatios.PERatio", startTime, endTime);

The preceding calls return fundamental data for the most recent trading days.

+

+

Defined Period of Time

+

+ To get the historical data of all the fundamental properties over specific period of time, call the History method with a start DateTimedatetime and an end DateTimedatetime.

+ To get the historical data of a single fundamental property over a specific period of time, call the GetFundamental method and include the name of a fundamental property.

+ To view the possible fundamental properties, see the Fundamental attributes in Data Point Attributes.

+ The start and end times you provide to these methods are based in the notebook time zone.

+

The preceding method returns the fundamental property values that are timestamped within the defined period of time.

-

The preceding method returns the fundamental data field values that are timestamped within the defined period of time.

diff --git a/04 Research Environment/03 Datasets/06 Equity Fundamental Data/05 Wrangle Data.html b/04 Research Environment/03 Datasets/06 Equity Fundamental Data/05 Wrangle Data.html

index fd19af450b..0c40523f70 100644

--- a/04 Research Environment/03 Datasets/06 Equity Fundamental Data/05 Wrangle Data.html

+++ b/04 Research Environment/03 Datasets/06 Equity Fundamental Data/05 Wrangle Data.html

@@ -1,17 +1,83 @@

You need some historical data to perform wrangling operations. To display pandas objects, run a cell in a notebook with the pandas object as the last line. To display other data formats, call the print method.

You need some historical data to perform wrangling operations. Use LINQ to wrangle the data and then call the Console.WriteLine method in a Jupyter Notebook to display the data.

-

The DataFrame index is the EndTime of the data sample. The columns of the DataFrame are the Equity Symbol objects.

+

DataFrame Objects

+

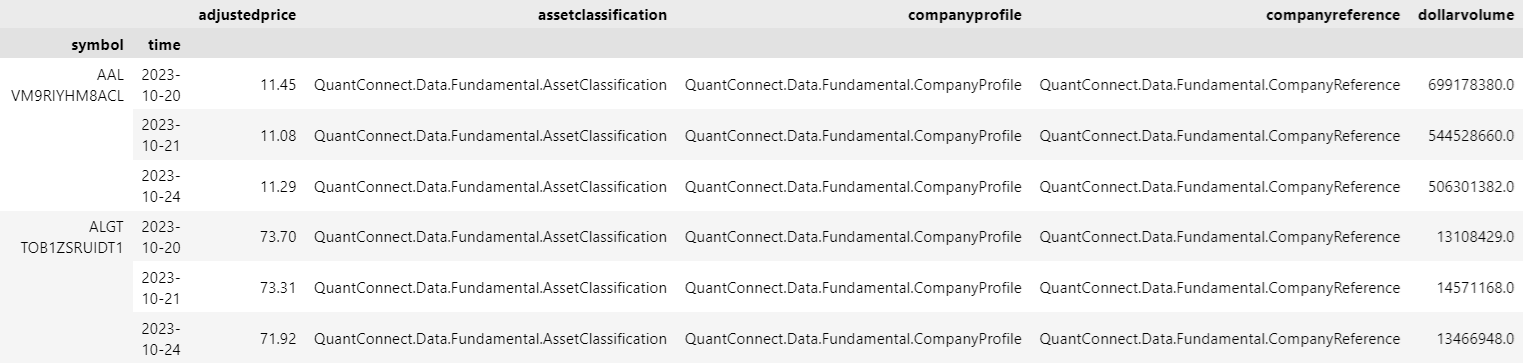

The History method returns a multi-index DataFrame where the first level is the Equity Symbol and the second level is the EndTime of the trading day. The columns of the DataFrame are the names of the fundamental properties. The following image shows the first 4 columns of an example DataFrame:

+

-

+

The GetFundamental method returns a DataFrame where the index is the EndTime of the trading day. The columns of the DataFrame are the Equity Symbol objects.

+

+

To select the historical data of a single Equity in the preceding DataFrame, index it with the Equity Symbol. Each history slice may not have data for all of your Equity subscriptions. To avoid issues, check if it contains data for your Equity before you index it with the Equity Symbol.

+

+

all_one_attribute_df[symbols[1]]

+

+

-

To get the fundamental data points for each Equity, iterate through the history request result.

+

Fundamental Objects

+

If you pass a Symbol to the History[Fundamental]History<Fundamental> method, run the following code to get the fundamental properties over time:

+

+

for fundamental in single_fundamental_history:

+ symbol = fundamental.Symbol

+ end_time = fundamental.EndTime

+ pe_ratio = fundamental.ValuationRatios.PERatio

+

foreach (var fundamental in singleFundamentalHistory) // Iterate trading days

+{

+ var endTime = fundamental.EndTime;

+ var peRatio = fundamental.ValuationRatios.PERatio;

+}

+

-

To select the historical data of a single Equity, index the DataFrame with the Equity Symbol. Each history slice may not have data for all of your Equity subscriptions. To avoid issues, check if it contains data for your Equity before you index it with the Equity Symbol.

+

If you pass a list of Symbol objects to the History[Fundamental]History<Fundamental> method, run the following code to get the fundamental properties over time:

+

+

for fundamental_dict in set_fundamental_history: # Iterate trading days

+ for symbol, fundamental in fundamental_dict.items(): # Iterate Symbols

+ end_time = fundamental.EndTime

+ pe_ratio = fundamental.ValuationRatios.PERatio

+

foreach (var fundamentalDict in setFundamentalHistory) // Iterate trading days

+{

+ foreach (var kvp in fundamentalDict) // Iterate Symbols

+ {

+ var symbol = kvp.Key;

+ var fundamental = kvp.Value;

+ var endTime = fundamental.EndTime;

+ var peRatio = fundamental.ValuationRatios.PERatio;

+ }

+}

+

+

Fundamentals Objects

+

If you request all fundamental properties for all US Equities with the History[Fundamentals]History<Fundamentals> method, run the following code to get the fundamental properties over time:

-

foreach (var slice in history)

+

for fundamentals_dict in all_fundamentals_history: # Iterate trading days

+ fundamentals = list(fundamentals_dict.Values)[0]

+ end_time = fundamentals.EndTime

+ for fundamental in fundamentals.Data: # Iterate Symbols

+ if not fundamental.HasFundamentalData:

+ continue

+ symbol = fundamental.Symbol

+ pe_ratio = fundamental.ValuationRatios.PERatio

+

foreach (var fundamentalsDict in allFundamentalsHistory) // Iterate trading days

{

+ var fundamentals = fundamentalsDict.Values.First().Data;

+ foreach (Fundamental fundamental in fundamentals) // Iterate Symbols

+ {

+ if (!fundamental.HasFundamentalData)

+ {

+ continue;

+ }

+ var endTime = fundamental.EndTime;

+ var symbol = fundamental.Symbol;

+ var peRatio = fundamental.ValuationRatios.PERatio;

+ }

+}

+

+

+

DataDictionary Objects

+

To get the fundamental data points for each Equity, iterate through the history request result.

+

+

foreach (var slice in allOneAttributeHistory)

+{

+ var endTime = slice.Time;

foreach (var symbol in symbols)

{

if (slice.ContainsKey(symbol))

@@ -20,15 +86,13 @@

}

}

}

-

history[symbols[1]]

-

-

You can also iterate through each data point in the slice.

-

foreach (var slice in history)

+

foreach (var slice in allOneAttributeHistory)

{

+ var endTime = slice.Time;

foreach (var kvp in slice)

{

var symbol = kvp.Key;

@@ -41,6 +105,5 @@

var symbol = symbols.Last();

-var values = history.Select(slice => slice[symbol]);

LinearAxis xAxis = new LinearAxis();

xAxis.SetValue("title", "Time");

LinearAxis yAxis = new LinearAxis();

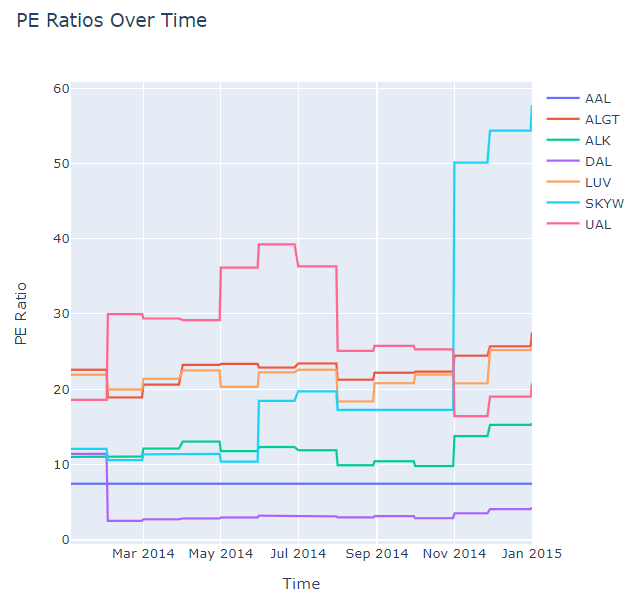

yAxis.SetValue("title", "PE Ratio");

-Title title = Title.init("AAPL & GOOG PE Ratio");

+Title title = Title.init("PE Ratios Over Time");

Layout layout = new Layout();

layout.SetValue("xaxis", xAxis);

@@ -38,9 +46,14 @@

Combine the charts and assign the Layout to the chart.

-

var chart = Plotly.NET.Chart.Combine(new []{chart1, chart2});

+

var chart = Plotly.NET.Chart.Combine(charts);

chart.WithLayout(layout);

+

+

Call the plot method on the history DataFrame.

+

+

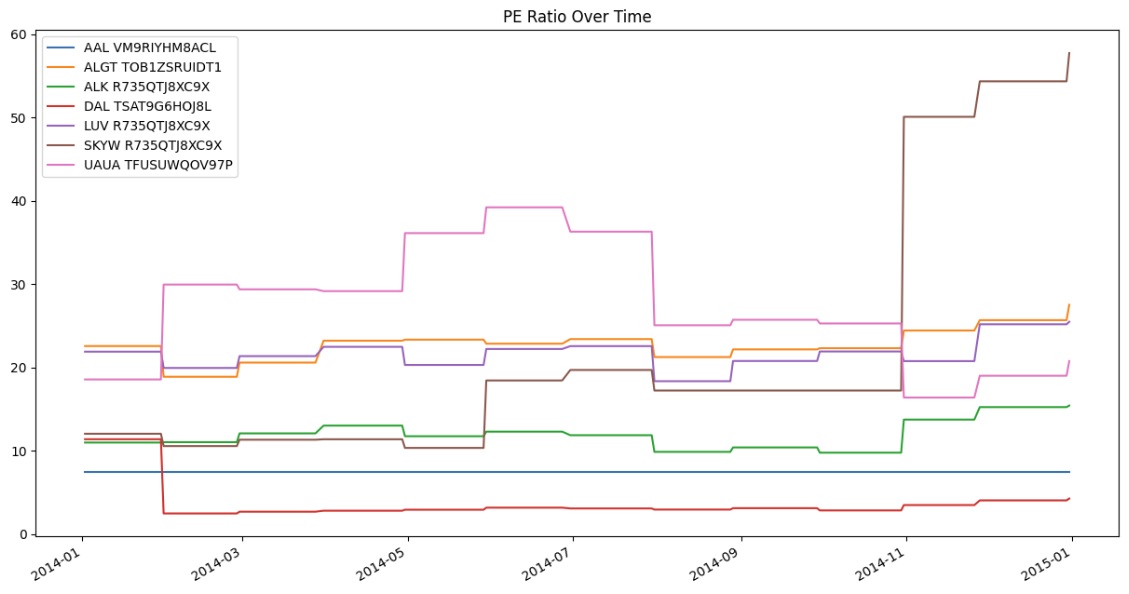

history.plot(title='PE Ratio Over Time', figsize=(15, 8))

+

Show the plot.

@@ -51,4 +64,4 @@

-

\ No newline at end of file

+

diff --git a/04 Research Environment/03 Datasets/06 Equity Fundamental Data/metadata.json b/04 Research Environment/03 Datasets/06 Equity Fundamental Data/metadata.json

index de647ed6fc..00bef67a8c 100644

--- a/04 Research Environment/03 Datasets/06 Equity Fundamental Data/metadata.json

+++ b/04 Research Environment/03 Datasets/06 Equity Fundamental Data/metadata.json

@@ -9,4 +9,4 @@

"og:site_name": "Equity Fundamental Data - QuantConnect.com",

"og:image": "https://cdn.quantconnect.com/docs/i/research-environment/datasets/equity-fundamental-data.png"

}

-}

\ No newline at end of file

+}

diff --git a/05 Lean CLI/05 Datasets/02 Downloading Data/01 Download By Ticker/02 Costs/02 US Equity.php b/05 Lean CLI/05 Datasets/02 Downloading Data/01 Download By Ticker/02 Costs/02 US Equity.php

index 5589297740..782986b6c3 100644

--- a/05 Lean CLI/05 Datasets/02 Downloading Data/01 Download By Ticker/02 Costs/02 US Equity.php

+++ b/05 Lean CLI/05 Datasets/02 Downloading Data/01 Download By Ticker/02 Costs/02 US Equity.php

@@ -54,13 +54,13 @@

Corporate fundamental data contains all the information on the underlying company of an Equity asset and the information in their financial statements. Since corporate data contains information not found in price and alternative data, adding corporate data to your trading strategies provides you with more information so you can make more informed trading decisions. Corporate fundamental data is available through the US Fundamental Data from Morningstar.

diff --git a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/03 ETF Constituents Universes/metadata.json b/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/03 ETF Constituents Universes/metadata.json

deleted file mode 100644

index 9d1e68696e..0000000000

--- a/08 Drafts/03 Writing Algorithms/12 Universes/03 Equity/03 ETF Constituents Universes/metadata.json

+++ /dev/null

@@ -1,12 +0,0 @@

-{