👍Contributions:

Ran Xin

Tian Yiping

Li Lingxiao

Environment requirements:

-

Environment: Python 3.6

-

Packages: tkinter : for UI, traceback: for capturing log, math: for some math calculations (root, square), scipy: for standard normal distribution density function, random: for generating Gaussian distribution random, numpy: for matrix operations

🔴To Run our option pricer, just put all the .py files in the same directory, and run gui.py.

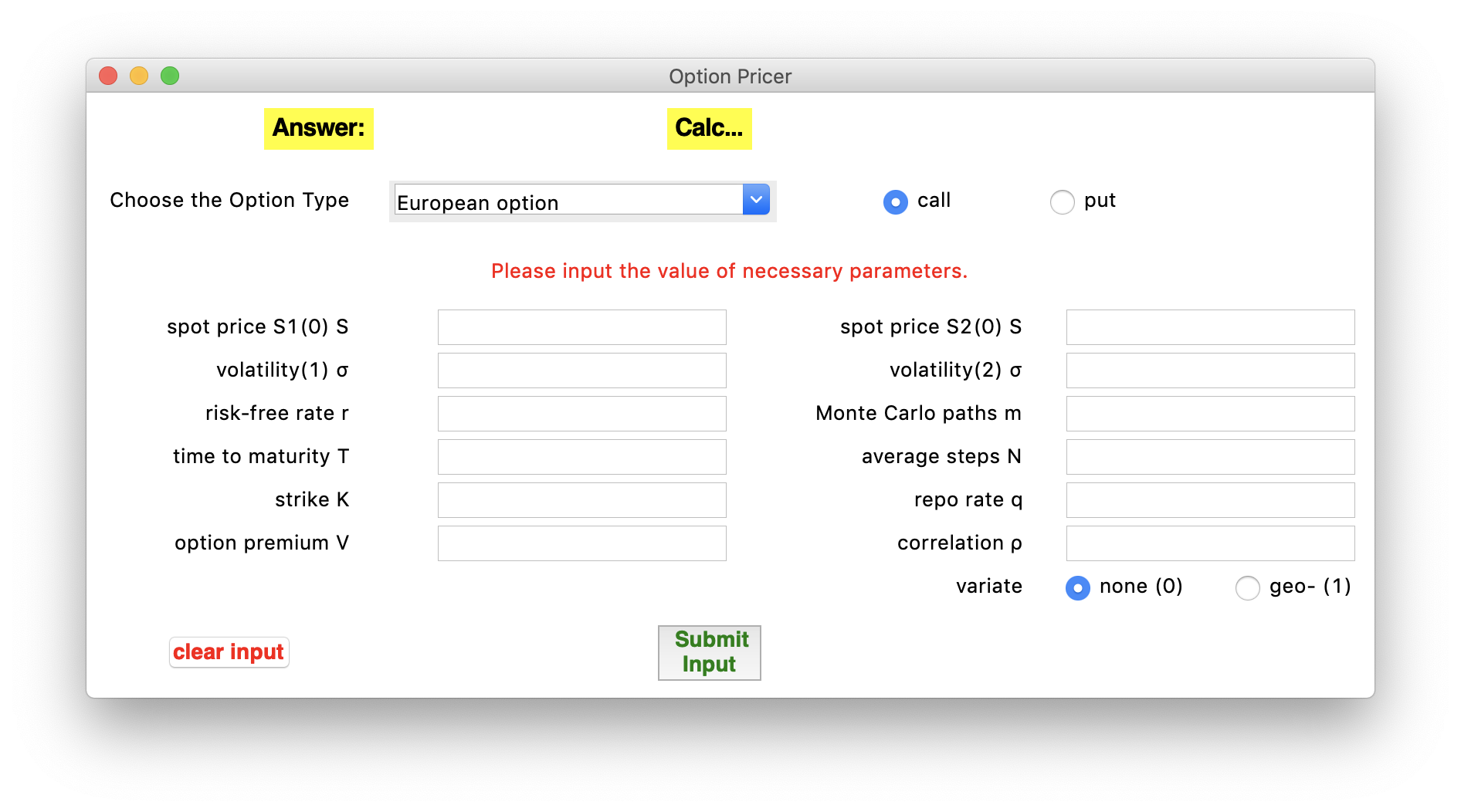

Using a simple python tkinter GUI libray to build a simple GUI Option Pricer:

-

Just like a Calculator the result answer shows in the above, highlight in yellow;

-

The second line is Option Type, it's a combo box, list all avaliable option types: European, American, Asian, Basket; Also you can click the radio button to choose call or put option.

-

The third line is alert information that informs you about which missing value you forget to input in order to make the calculation. We simply extract the error traceback message to achieve this.

-

In the middle area is input value field, all the input parameters should be input here, left-hand side is most commonly input one, right-hand side is less common and also symmetric.

-

In the bottom center (green) its a submit button, and the bottom left (red) is clear all input button.

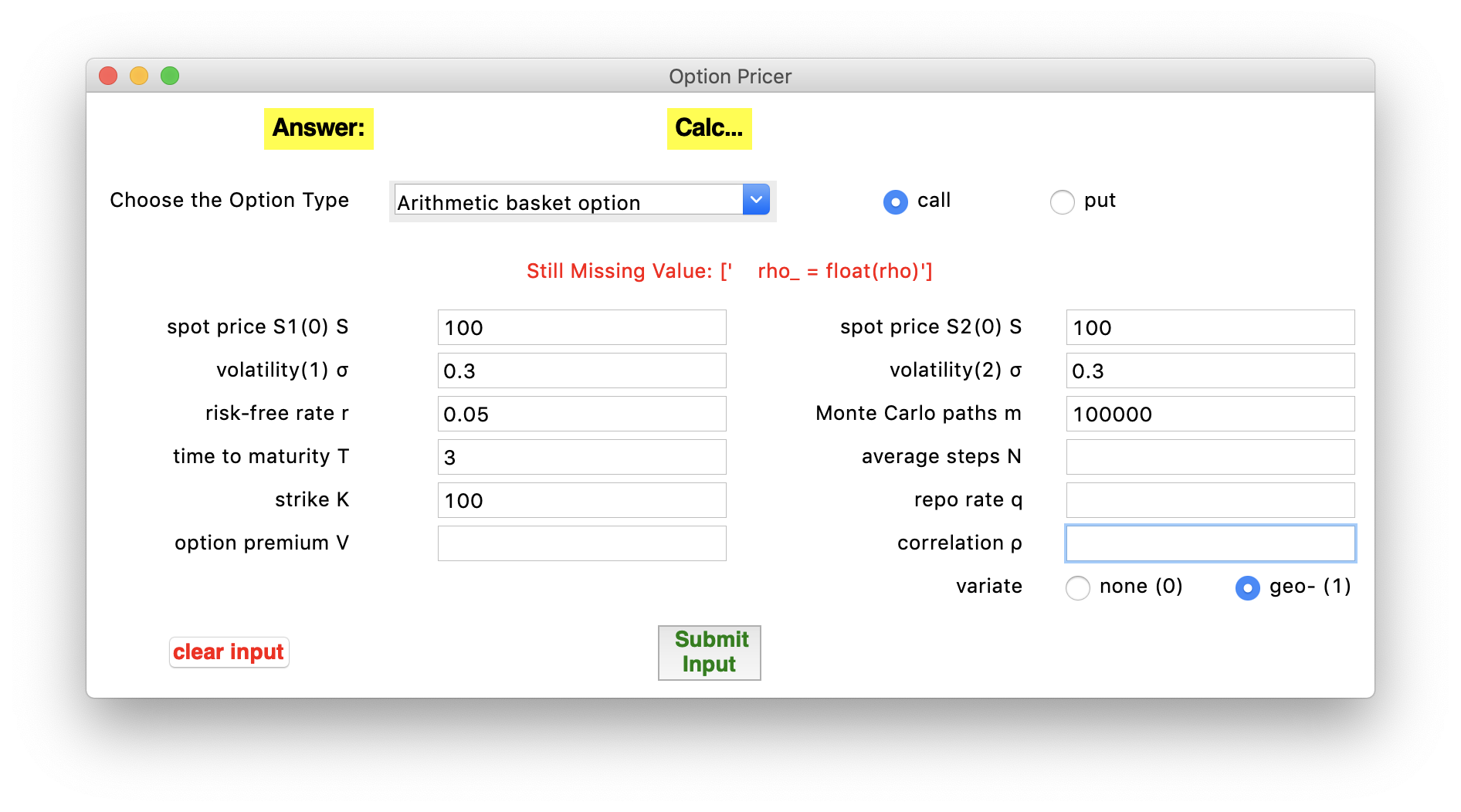

Choose option type, here we select "Arithmetic basket option", call, input all the needed parameter, with variate:

if we forget input the correlation ρ , click submit will be informed,

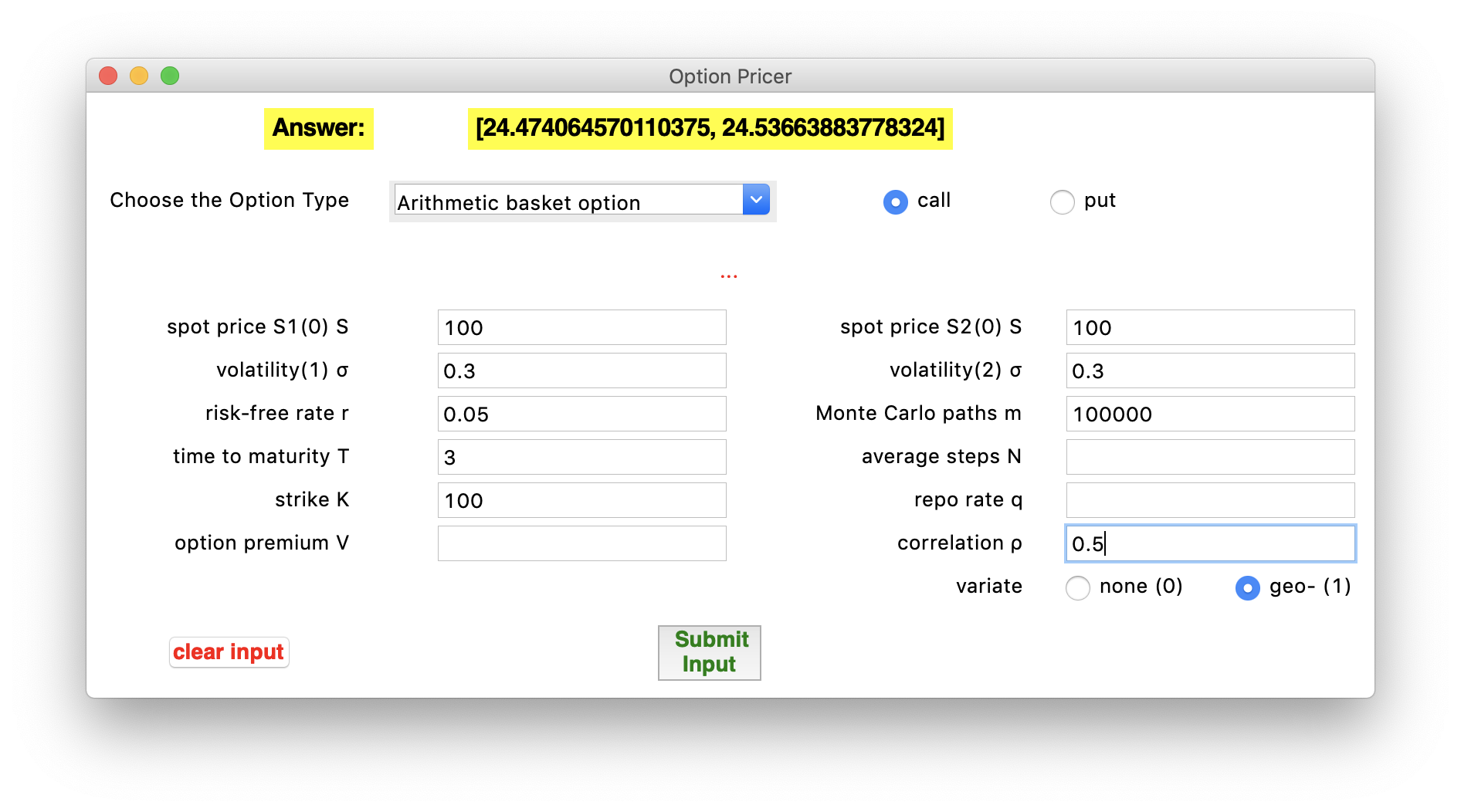

after all correct, the answer will be calculated and display in above.

parameter in code

spot price S, volatility sigma, risk-free rate r, time to maturity T, strike K, option premium V, Monte Carlo paths path, average steps n, repo rate q, correlation rho

european.py (S, sigma, r, T, K, type, q)

Using Lecture 3 Black-Scholes Formulas: with BS-PDE & Call-Put Parity

volatility.py (S, S_true, r, T, K, q, type)

Follow the formulas in "lecture 4" using Newton Method to solve the problem which converges quickly:

american.py (S, sigma, r, T, K, n, type)

There is no closed formular, so we use bionominal tree in "lecture 6" to solve it. First step is to iterate the bionominal tree and calculate the stock price in each node. Second step is to backtrack the tree and calculate the price of call/put options.

baskt_geometric.py (S1, S2, sigma1, sigma2, rho, r, T, K, option_type)

Follow the formulas described in mathematical background in "assignment 3" geometric Brownian motion, we can figure out the call or put geometric basket option.

basket_arithmetic.py (path, S1, S2, sigma1, sigma2, rho, r, T, K, option_type, variate)

For arithmetic option price, there is no closed-form formulas so we need to use Monte Carlo to simulate the stock price. We use the method proved in assignment 2 (2.1) to generate two random varibles with correlation coefficient σ. Then, similar to Asian option, we can calculate the basket option price (95% confidence interval) with or without control variate.

Rest is similar to Asian-Arithmetic, 2 drift, 2 growthFactor. simulate multiple times output the 95% confidence interval.

asian_geometric.py (S, sigma, r, T, K, n, option_type)

There is a closed formular in "lecture 5" we can simply implement it.

asian_arithmetic.py (path, S, sigma, r, T, K, n, option_type, variate)

There is no closed-form formulas so we need to use Monte Carlo to simulate it.

Then calculate the mean, std, cov of the payoff, simulate multiple times output the 95% confidence interval.

how each parameter affects the option price

r = 0.05, T = 3, and S(0) = 100. paths in Monte Carlo simulation is m = 100, 000. RandomSeed(1234)

| σ | K | n | Type | Geometric | Arithmetic | Arithmetic(variate) |

|---|---|---|---|---|---|---|

| 0.3 | 100 | 50 | Put | 8.482 | 7.681~7.818 | 7.799~7.807 |

| 0.3 | 100 | 100 | Put | 8.431 | 7.667~7.804 | 7.747~7.756 |

| 0.4 | 100 | 50 | Put | 12.558 | 11.125~11.304 | 11.277~11.292 |

| 0.3 | 100 | 50 | Call | 13.259 | 14.639~14.927 | 14.714~14.736 |

| 0.3 | 100 | 100 | Call | 13.138 | 14.482~14.768 | 14.598~14.620 |

| 0.4 | 100 | 50 | Call | 15.759 | 18.072~18.476 | 18.181~18.222 |

| Geometric Asian | Call option | Put option |

|---|---|---|

| volatility (σ) ↑ | ↑↑ | ↑↑ |

| average steps (n) ↑ | ↓ | ↓ |

| Arithmetic Asian | Call option | Put option |

|---|---|---|

| volatility (σ) ↑ | ↑↑ | ↑↑ |

| average steps (n) ↑ | ↓ | ↓ |

| S1(0) | S2(0) | K | σ1 | σ2 | ρ | Type | Geometric | Arithmetic | Arithmetic(variate) |

|---|---|---|---|---|---|---|---|---|---|

| 100 | 100 | 100 | 0.3 | 0.3 | 0.5 | Put | 11.491 | 10.469~10.658 | 10.563~10.587 |

| 100 | 100 | 100 | 0.3 | 0.3 | 0.9 | Put | 12.622 | 12.281~12.492 | 12.426~12.431 |

| 100 | 100 | 100 | 0.1 | 0.3 | 0.5 | Put | 6.586 | 5.479~5.593 | 5.508~5.525 |

| 100 | 100 | 80 | 0.3 | 0.3 | 0.5 | Put | 4.711 | 4.214~4.325 | 4.247~4.262 |

| 100 | 100 | 120 | 0.3 | 0.3 | 0.5 | Put | 21.289 | 19.712~19.980 | 19.867~19.900 |

| 100 | 100 | 100 | 0.5 | 0.5 | 0.5 | Put | 23.469 | 20.885~21.178 | 21.054~21.110 |

| 120 | 100 | 100 | 0.3 | 0.3 | 0.5 | Put | 8.915 | 7.975~8.144 | 8.043~8.068 |

| 120 | 120 | 100 | 0.3 | 0.3 | 0.5 | Put | 6.736 | 6.047~6.195 | 6.095~6.115 |

| 100 | 100 | 100 | 0.3 | 0.3 | 0.5 | Put r=0.1 | 6.423 | 5.782~5.915 | 5.828~5.846 |

| 100 | 100 | 100 | 0.3 | 0.3 | 0.5 | Put T=1 | 8.257 | 7.774~7.914 | 7.845~7.856 |

| 100 | 100 | 100 | 0.3 | 0.3 | 0.5 | Call | 22.102 | 24.334~24.818 | 24.461~24.523 |

| 100 | 100 | 100 | 0.3 | 0.3 | 0.9 | Call | 25.878 | 26.223~26.775 | 26.351~26.364 |

| 100 | 100 | 100 | 0.1 | 0.3 | 0.5 | Call | 17.924 | 19.296~19.641 | 19.414~19.451 |

| 100 | 100 | 80 | 0.3 | 0.3 | 0.5 | Call | 32.536 | 35.227~35.765 | 35.352~35.415 |

| 100 | 100 | 120 | 0.3 | 0.3 | 0.5 | Call | 14.685 | 16.434~16.854 | 16.559~16.617 |

| 100 | 100 | 100 | 0.5 | 0.5 | 0.5 | Call | 28.449 | 34.598~35.537 | 34.865~35.071 |

| 120 | 100 | 100 | 0.3 | 0.3 | 0.5 | Call | 28.753 | 31.815~32.377 | 31.946~32.024 |

| 120 | 120 | 100 | 0.3 | 0.3 | 0.5 | Call | 36.683 | 39.832~40.468 | 39.979~40.055 |

| 100 | 100 | 100 | 0.3 | 0.3 | 0.5 | Call r=0.1 | 29.023 | 31.588~32.112 | 31.710~31.773 |

| 100 | 100 | 100 | 0.3 | 0.3 | 0.5 | Call T=1 | 12.015 | 12.649~12.889 | 12.715~12.733 |

| Geometric Basket | Call option | Put option |

|---|---|---|

| spot price (S1) ↑ | ↑ | ↓ |

| spot price (S1) ↑ (S1)↑ | ↑↑ | ↓↓ |

| strike (K) ↓ | ↑ | ↓ |

| maturity (T) ↓ | ↓ | ↓ |

| risk free rate (r) ↑ | ↑ | ↓ |

| volatility (σ1) ↓ | ↓ | ↓ |

| volatility (σ1) ↑ volatility (σ2) ↑ | ↑ | ↑ |

| correlation coefficient (ρ) ↑ | ↑ | ↑ |

| Arithmetic Basket | Call option | Put option |

|---|---|---|

| spot price (S) ↑ | ↑ | ↓ |

| spot price (S1) ↑ (S1)↑ | ↑↑ | ↓↓ |

| strike (K) ↓ | ↑ | ↓ |

| maturity (T) ↓ | ↓ | ↓ |

| risk free rate (r) ↑ | ↑ | ↓ |

| volatility (σ) ↓ | ↓ | ↓ |

| volatility (σ1) ↑ volatility (σ2) ↑ | ↑ | ↑ |

| correlation coefficient (ρ) ↑ | ↑ | ↑ |

| S1(0) | K | σ1 | r | T | Type | European |

|---|---|---|---|---|---|---|

| 100 | 100 | 0.2 | 0.01 | 0.5 | call | 5.876024 |

| 100 | 120 | 0.2 | 0.01 | 0.5 | call | 0.774138 |

| 100 | 120 | 0.2 | 0.01 | 1 | call | 8.433318 |

| 100 | 100 | 0.3 | 0.01 | 0.5 | call | 8.677645 |

| 100 | 100 | 0.2 | 0.02 | 0.5 | call | 6.120654 |

| 100 | 100 | 0.2 | 0.01 | 0.5 | put | 5.377272 |

| 100 | 120 | 0.2 | 0.01 | 0.5 | put | 20.17563 |

| 100 | 120 | 0.2 | 0.01 | 1 | put | 7.438302 |

| 100 | 100 | 0.3 | 0.01 | 0.5 | put | 8.178893 |

| 100 | 100 | 0.2 | 0.02 | 0.5 | put | 5.125637 |

| European | Call option | Put option |

|---|---|---|

| strike (K) ↑ | ↓↓ | ↑↑ |

| maturity (T) ↑ | ↑ | ↓ |

| risk free rate (r) ↑ | ↑ | ↓ |

| volatility (σ) ↑ | ↑ | ↓ |

| S1(0) | K | σ1 | r | T | Type | European |

|---|---|---|---|---|---|---|

| 100 | 100 | 0.2 | 0.01 | 0.5 | call | 5.861975 |

| 100 | 120 | 0.2 | 0.01 | 0.5 | call | 0.776743 |

| 100 | 100 | 0.2 | 0.01 | 1 | call | 8.413504 |

| 100 | 100 | 0.3 | 0.01 | 0.5 | call | 8.656601 |

| 100 | 100 | 0.2 | 0.02 | 0.5 | call | 6.106614 |

| 100 | 100 | 0.2 | 0.01 | 0.5 | put | 5.363223 |

| 100 | 120 | 0.2 | 0.01 | 0.5 | put | 20.17824 |

| 100 | 100 | 0.2 | 0.01 | 1 | put | 7.418488 |

| 100 | 100 | 0.3 | 0.01 | 0.5 | put | 8.157849 |

| 100 | 100 | 0.2 | 0.02 | 0.5 | put | 5.111597 |

| American | Call option | Put option |

|---|---|---|

| strike (K) ↑ | ↓↓ | ↑↑ |

| maturity (T) ↑ | ↑ | ↓ |

| risk free rate (r) ↑ | ↑ | ↓ |

| volatility (σ) ↑ | ↑ | ↓ |